Smart Ways to Pay Off Your Car Loan Faster in 2025: Discover Proven Strategies to Improve Financial Freedom

Smart Ways to Pay Off Your Car Loan Faster

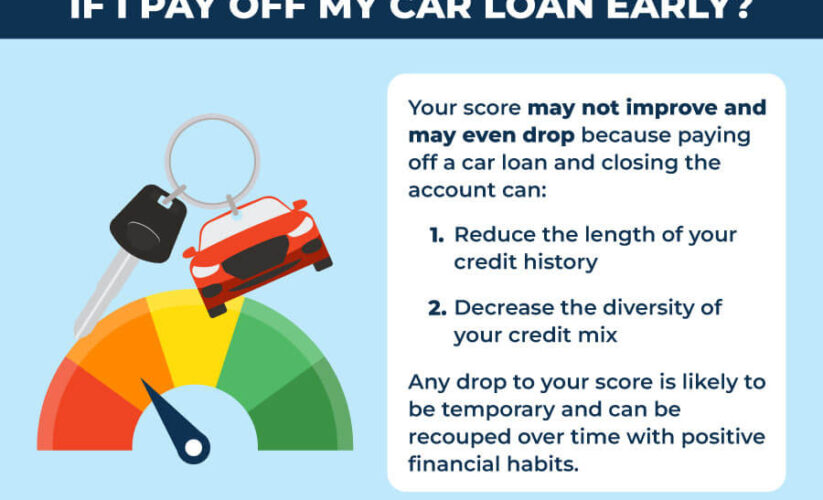

Understanding Car Loan Terms

To effectively **pay off your car loan faster**, it’s essential to have a solid grasp of your car loan terms. Many borrowers overlook the details of their loan agreements, which can result in missed opportunities to reduce their loan burden. Key elements such as the **interest rate**, loan duration, and repayment schedule significantly affect your monthly payments and total loan cost. For instance, understanding the **total cost of the loan** allows you to pinpoint how much extra you could save by making higher payments. Additionally, familiarize yourself with terms such as **amortization** to better understand how your payments are applied towards both principal and interest.

Loan Appreciation Concepts

The concept of **car equity** comes into play when understanding your loan. As you make payments, your equity grows while the amount owed on the loan decreases. This can be particularly beneficial if you choose to sell your vehicle or trade it in to **pay off your loan** faster. Evaluating your car’s market value in relation to your remaining balance can help you determine the best course of action for leveraging that equity for quicker loan repayment.

Navigating Interest Rates

The **impact of interest rates** on the overall cost of your car loan cannot be understated. A small difference in the interest rate can lead to significant savings over the lifespan of your loan. Negotiating a **lower interest rate** is one of the most effective strategies to **accelerate car loan repayment**. When you improve your credit score or present a solid payment history, lenders may be willing to offer a rate reduction. Utilizing online **car loan payoff calculators** can also help you visualize how different rates affect your total payment and interest accrued.

Effective Payment Strategies

When looking to **accelerate car loan repayment**, consider strategic payment methods. Implementing a well-thought-out plan can make your journey toward financial freedom smoother and more efficient. For instance, making **extra payments on your car loan** whenever possible chips away at the principal faster, thus reducing the amount of interest paid over time. This is a surefire way to stimulate your journey towards complete loan satisfaction, especially if coupled with other strategies.

Biweekly Payments

Instead of traditional monthly payments, opting for **biweekly payments** can significantly reduce your unpaid principal balance over time. Paying half of your monthly payment every two weeks results in an additional payment each year, preventing high-interest accumulation. This method allows for the **streamlining of the loan repayment process**, ultimately leading to exponential savings on interest. Integrating **automatic payments** can also enforce this habit and maintain consistent progress towards your goals.

Utilizing Savings Wisely

If you maintain an emergency fund, consider periodically using it to make **extra payments on your car loan**. For example, allocating any unexpected **tax refunds** or bonuses towards your vehicle’s loan principal will considerably advance your repayment schedule. However, ensure you have sufficient funds to manage emergencies before dedicating all savings towards a loan. This balance between **building financial health** and responsibly managing debt is crucial for long-term stability.

Refinancing and Loan Consolidation

Exploring **loan refinancing options** may present a practical route to faster repayment. If your credit score has improved or market interest rates have dipped since you acquired the loan, refinancing could allow you to secure a significantly lower rate. Moreover, consolidating multiple types of debt—a process called ** debt consolidation **—into a vehicle loan can simplify managing your payments while possibly securing a lower total interest rate.

Benefits of Loan Consolidation

Often, **car loan consolidation** streamlines your repayments into one manageable installment, which simplifies budgeting and tracking your payments. Ensuring you adhere to a defined **car loan repayment plan** will not only provide clarity on how much you owe monthly but will also serve to stabilize your finances. Establishing a concrete plan is essential when juggling multiple loan types, such as student loans or credit cards.

Negotiating Better Terms

Negotiation is crucial in achieving financial excellence in your loan journey. Discussing loan terms with your **lender** can offer opportunities to reduce overall costs, such as **lowering your monthly interest rate** or extending your loan to facilitate smaller payments. However, this option may backfire if not weighed against the accrual of interest due to the extended payment timeline. Understanding your current loan terms aids in determining the best negotiating strategies for possible value enhancement.

Budgeting Tactics and Financial Planning

The precise management of your expenses can be the cornerstone of an effective **financial strategy** to **pay off your car loan faster**. Implementing **smart budgeting techniques** ensures you can allocate sufficient funds towards your car payments while balancing living expenses. Assessing your cash flow allows you to identify areas where you can economize, which contributes to more substantial monthly loan commitments.

Creating a Monthly Financial Overview

An organized **monthly financial overview** provides insights detailing how much of your income is ear-marked for **car payments**, **savings**, and other living expenditures. Utilizing tools, such as budgeting apps, can facilitate tracking your expenses effectively while implementing cost-cutting measures where necessary. Awareness of your financial habits also promotes increased **financial discipline for car loans**, allowing for better management and readiness to pay off debts.

Keeping Track of Payments

Implement systems to monitor your **loan payment notifications** and establish a payment calendar to stay ahead. Knowing your payment due dates and their amounts fosters a sense of accountability. Using a **car loan payment plan** not only enhances your organization but could also inspire you to make additional payments when feasible, ensuring progressive steps toward **financial freedom from car loans**.

Key Takeaways

- Thoroughly understanding car loan terms empowers strategic payment choices.

- Employing biweekly payment methods can effectively reduce interest accrued over time.

- Loan refinancing, when applicable, offers cost-effective pathways to quicker debt freedom.

- Implementing practical budgeting strategies ensures ample funds to tackle monthly repayments.

- Negotiating with lenders can yield beneficial payment terms that align with your financial goals.

FAQ

1. How can I negotiate for a lower interest rate on my car loan?

Start by reviewing your credit report and improving your credit score to reflect better financial stability. Compare offers from various lenders and use these as leverage when discussing terms with your current lender. Presenting a strong payment history can also bolster your chances of securing a **lower interest rate**, leading to substantial savings in the long run.

2. What are the benefits of making extra payments on my car loan?

Making **extra payments on your car loan** not only decreases the principal faster but also reduces the overall interest accrued over the lifespan of the loan. This can lead you to own your vehicle outright sooner and increase financial freedom by freeing up funds for other investments or expenses.

3. What is the debt snowball method and how can it be applied to car loans?

The **debt snowball method** involves focusing on paying off the smallest debts first while making minimum payments on larger debts. This can be motivating as it allows borrowers to eliminate smaller obligations quickly. For car loans, this method can be applied by targeting the car loan alongside any supplementary debts, creating momentum as you free yourself from additional financial commitments.

4. Can I use my tax refunds to help with my car loan payments?

Absolutely! Applying your **tax refunds** directly to your car loan can significantly accelerate repayment. This approach helps decrease your principal balance and reduces the total interest paid on the loan, enabling you to achieve financial freedom more swiftly.

5. What are the risks of refinancing my car loan?

While **loan refinancing** can lead to lower monthly payments, it’s vital to carefully analyze potential costs and drawbacks. There may be fees associated with refinancing, and if the new interest rate is higher than your current one, it could result in paying more over time. Ensure to calculate the potential **savings versus costs** before making any decisions.

6. How can I manage my overall financial health while paying off a car loan?

Building an effective financial strategy involves creating and sticking to comprehensive budgets while actively seeking to **reduce your debt-to-income ratio**. Consider employing tips for **financial planning**, savings strategies, and disciplined spending habits that prioritize loan repayments but also account for everyday expenses and savings for future needs.

7. Is selling my car a viable option to pay off the loan quickly?

Selling your car can be a **viable option** to pay off your loan faster if the market value exceeds your remaining balance. This approach can eliminate the loan altogether and allows you to reinvest in a more affordable vehicle or redirect the funds towards savings or other debt obligations. Weighing options carefully based on your financial status is essential before taking such a step.